AeroVironment ($AVAV) Restates Q3: Space Goodwill Impairment Revised 59% Higher to $240.7M Just Months After the $4B+ BlueHalo Deal — Plus a Material Weakness

AVAV's blistering top-line growth was bought, not earned — and within three quarters of paying $4B+ for BlueHalo it wrote down $240.7M of the Space unit's goodwill, then had to restate that charge 59% higher because its own controls over the calculation were a material weakness. The growth narrative is intact; the deal economics and the control environment are not.

AVAV

10-QCautiousAeroVironment, Inc.

AVAV's blistering top-line growth was bought, not earned — and within three quarters of paying $4B+ for BlueHalo it wrote down $240.7M of the Space unit's goodwill, then had to restate that charge 59% higher because its own controls over the calculation were a material weakness. The growth narrative is intact; the deal economics and the control environment are not.

⚠ Major Risks

- •Newly identified material weakness in internal control over financial reporting tied specifically to the goodwill impairment analysis; management concluded disclosure controls and procedures were ineffective as of January 31, 2026, and the prior evaluation can no longer be relied upon.

- •A $240,708K goodwill impairment hit the Space reporting unit within roughly nine months of the May 1, 2025 BlueHalo acquisition — yet $2,372,312K of goodwill plus $925,925K of intangibles (~61% of the $5.36B balance sheet) remain exposed to further write-downs.

- •Extreme U.S. government concentration: $1,158,722K of the $1,335,229K nine-month revenue (~87%) is U.S. government, subject to DCAA cost audits that could disallow incurred costs and to federal budget risk.

- •Leverage ballooned post-deal: long-term debt rose to $727,877K from $30,000K (including convertible notes), funded alongside heavy equity dilution, with credit-agreement leverage and fixed-charge coverage covenants now in play.

- •Operating cash burn of $173,917K for nine months, driven by a $142,088K build in unbilled receivables and a $92,721K inventory build that are outrunning cash collections.

🔍 Accounting Red Flags

- ▲Formal restatement (Form 10-Q/A): the Space-unit goodwill impairment was understated because the carrying value omitted goodwill from acquired deferred tax assets/liabilities, increasing the charge by $89,402K — from $151,306K as originally reported to $240,708K.

- ▲Material weakness in ICFR over the preparation and review of the goodwill impairment analysis; net loss was understated by $87,272K and diluted loss per share by $1.75 (quarter) / $1.79 (nine months) in the original filing.

- ▲Impairing a freshly acquired unit within the same fiscal year as the acquisition raises purchase-price-allocation and valuation concerns over the remaining $2,372,312K of goodwill.

- ▲Unbilled receivables and retentions jumped to $528,557K from $290,009K with 73% of nine-month revenue recognized over time, concentrating reliance on management's contract cost/revenue estimates and lengthening cash conversion.

- ▲Income taxes receivable surged to $43,031K from $622K and a tax benefit was booked against the losses, magnifying the gap between reported results and cash.

💰 Cash Flow Quality

Despite enormous non-cash add-backs, the company burned $173,917K of operating cash over nine months as working capital consumed the business's growth.

- •Net cash used in operating activities was $(173,917)K versus $(1,054)K a year earlier, even after adding back $240,708K of goodwill impairment and $202,960K of depreciation/amortization.

- •Working-capital drains dominated: unbilled receivables $(142,088)K, inventories $(92,721)K, income taxes receivable $(38,646)K, accounts receivable $(19,892)K.

- •Financing provided $1,647,210K (incl. $968,515K of share issuance and $726,944K of convertible debt) and investing used $(1,224,921)K, largely $(844,586)K for BlueHalo — i.e., the cash buffer is borrowed/issued, not earned.

- •Interest paid rose to $12,535K from $1,196K, reflecting the new debt load.

🏰 Competitive Position

A specialized, incumbent defense-technology supplier with a broad multi-domain portfolio and sticky government programs, but dependent on U.S. budgets and now digesting an expensive, partly impaired acquisition.

- +Leading position in UAS, loitering munitions and precision strike, expanded by BlueHalo into space, cyber, directed energy and counter-UAS.

- +Funded backlog of approximately $1,120,675K, with ~39% expected to convert in fiscal 2026.

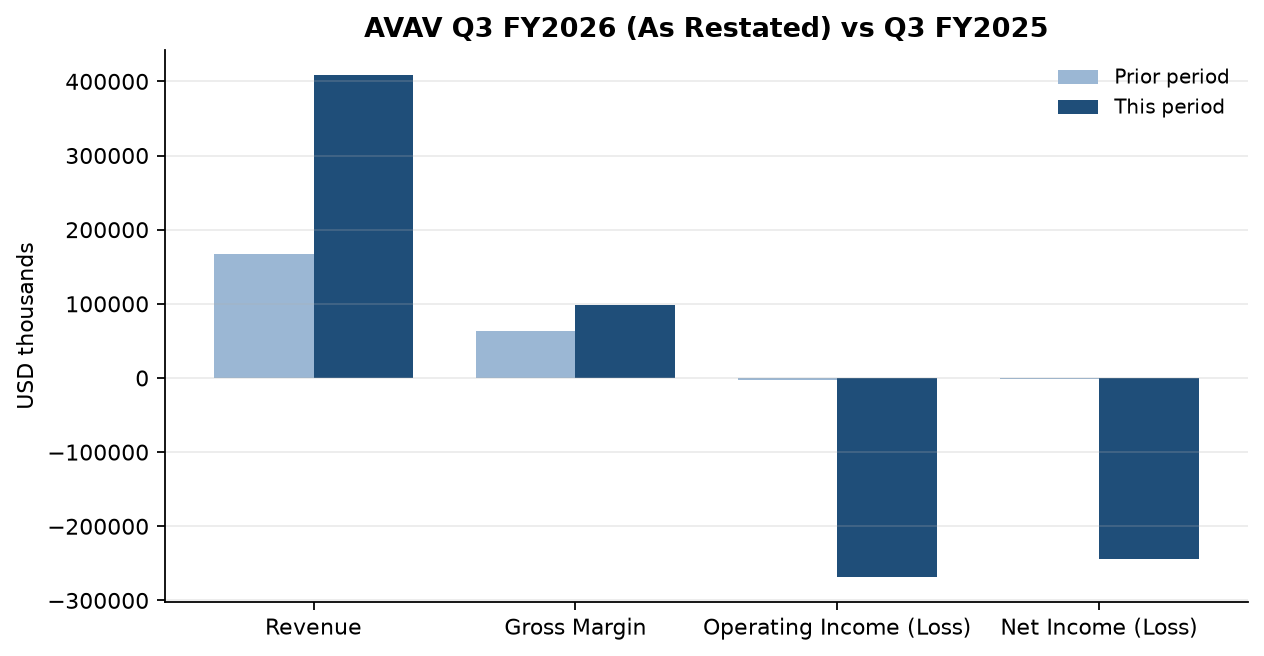

- +Top-line scale jumped sharply: Q3 revenue $408,045K (+143%) and nine-month revenue $1,335,229K (+145%).

- +Diversified contract mix (FFP $880,854K, Cost Plus $346,080K, T&M $108,295K) and a $1B uncommitted receivables-factoring facility for liquidity.

- -~87% U.S. government revenue concentration and exposure to DCAA cost disallowances.

- -Just impaired the acquired Space unit's goodwill by $240,708K — evidence of overpayment or a weaker-than-priced asset.

- -Material weakness in financial controls undermines confidence in management's estimates.

- -Negative operating cash flow, elevated leverage, and ~77% share-count increase (28.3M to 49.9M) erode per-share economics.

The consensus read is that AeroVironment is the breakout defense-tech compounder: quarterly revenue surged 143% to $408.0M and nine-month revenue 145% to $1.34B, backed by a $1.12B funded backlog and a newly multi-domain portfolio after swallowing BlueHalo. Invert it, and the same numbers tell you the growth was purchased rather than generated — AV issued roughly 21.5M shares (lifting the count from 28M to 50M) and took on $728M of new debt to fund the ~$845M cash and ~$2.64B stock cost of the deal, then impaired $240.7M of the acquired Space unit's goodwill within nine months of closing.

The tell isn't the impairment itself — it's that management couldn't compute it. The restatement raised the charge by $89.4M, from $151.3M to $240.7M, because the Space reporting unit's carrying value left out goodwill arising from acquired deferred taxes. That mechanical miss was serious enough to be declared a material weakness and to render disclosure controls 'ineffective.' When an acquirer writes down a freshly bought business and simultaneously fumbles the very estimate that exposes it, both the purchase-price allocation and the remaining $2.37B of goodwill (plus $925.9M of intangibles — together ~61% of assets) deserve hard scrutiny.

In plain English: they paid top dollar for BlueHalo, part of it was demonstrably worth less almost immediately, and the finance organization wasn't in control of the math that revealed it. Underneath, the core business is consuming cash — operating cash flow was negative $173.9M for nine months as unbilled receivables (+$142.1M) and inventory (+$92.7M) outgrew collections, with the cash cushion supplied by debt and equity issuance.

What to watch is the fiscal-2026 10-K (year ended April 30, 2026): whether the Space unit absorbs further impairment, whether the material weakness is remediated, and whether the swelling unbilled receivables convert into cash. Goodwill and intangibles are the swing factor on this balance sheet.

Want this on every stock you own?

Run instant AI analysis of any 10-K or 10-Q from EDGAR — major risks, red flags, cash flow quality, and moat — with Value of Stock Premium.

This analysis is generated from the filing text and is for educational purposes only — not financial advice. Always do your own research before investing.