Commercial Metals ($CMC): the swing to a $443M profit is mostly a vanished $358M litigation charge — while a $2.5B debt-funded precast bet tripled goodwill and quadrupled interest

The headline reversal from a $67M loss to record $443M nine-month earnings is real in dollars but largely mechanical — the absence of last year's $358.5M litigation charge plus a sub-8% effective tax rate — while a $2.5B debt-funded precast acquisition has tripled goodwill and quadrupled interest, shifting CMC from a clean balance sheet to a leveraged integration story.

CMC

10-QCautiousCommercial Metals Company

The headline reversal from a $67M loss to record $443M nine-month earnings is real in dollars but largely mechanical — the absence of last year's $358.5M litigation charge plus a sub-8% effective tax rate — while a $2.5B debt-funded precast acquisition has tripled goodwill and quadrupled interest, shifting CMC from a clean balance sheet to a leveraged integration story.

⚠ Major Risks

- •Sharp leverage increase: long-term debt rose from $1.31B to $3.31B (2.5x) after ~$2.0B of new 5.750%–6.000% senior notes to fund acquisitions; quarterly interest expense quadrupled to $40.2M (from $10.9M).

- •Integration and goodwill-concentration risk from the ~$2.5B Foley ($1.84B) and CP&P ($675M) precast acquisitions, which added ~$1.75B of goodwill on still-preliminary purchase accounting.

- •An unresolved $373.5M accrued contingent litigation-related loss remains on the balance sheet (litigation expense was $358.5M in the prior nine months).

- •European profitability leans on Poland energy-cost government assistance ($36.0M for nine months, down from $48.1M) booked as a reduction to cost of goods sold — a shrinking, non-operational margin prop.

- •Commodity cyclicality: results depend on steel/scrap pricing, energy costs and PLN/FX exposure, which the Company manages with commodity and foreign-exchange derivatives.

🔍 Accounting Red Flags

- ▲Net-income quality flattered by an abnormally low effective tax rate — 7.9% for nine months and 8.4% in Q3 — versus a normal corporate rate, aided by tax-deductible acquisition goodwill (Foley goodwill deductible over 15 years).

- ▲Goodwill ballooned 5.5x to $2.14B (~22% of total assets); $1.33B (≈72%) of Foley's $1.84B price landed as goodwill, and allocations remain preliminary within the one-year measurement period, with a prior-period error-correction adjustment already recorded.

- ▲Government grants of $36.0M are recognized as reductions to cost of goods sold rather than below the operating line, inflating reported gross margin.

- ▲A $2.7M purchase-accounting inventory step-up was run through cost of goods sold as acquired inventory was sold.

💰 Cash Flow Quality

Operating cash flow improved to $603.0M, but a $195.1M working-capital drag and $404.3M of capex left only modest free cash flow against a $2.5B acquisition funded by debt and cash.

- •Net cash from operations rose to $603.0M from $399.9M, driven by the swing to net earnings.

- •Changes in operating assets and liabilities were a $195.1M use of cash (receivables and inventory up, partly acquisition-related).

- •Capital expenditures of $404.3M imply roughly $199M of free cash flow for the nine months.

- •Acquisitions of $2,516.1M were funded by $1,985.0M of new long-term debt plus cash; total cash fell $483.5M to $559.8M.

- •Depreciation and amortization jumped to $282.7M (from $213.4M) and cash paid for interest nearly doubled to $71.4M.

🏰 Competitive Position

A low-cost, vertically integrated EAF rebar producer with regional scale now diversifying into precast, but its core product remains a cyclical commodity.

- +Vertical integration from scrap recycling through electric-arc-furnace steelmaking to downstream fabrication and now precast concrete.

- +Leading North American rebar/long-products position tied to U.S. infrastructure and construction demand.

- +New Construction Solutions Group/precast platform (Foley, CP&P) adds higher-value, differentiated mission-critical site-infrastructure products.

- -Core steel is a price-taking commodity exposed to scrap and energy costs and import competition.

- -European (Poland) profitability depends on government energy subsidies that are declining.

- -Newly elevated leverage and $2.1B of acquisition goodwill raise financial and integration risk.

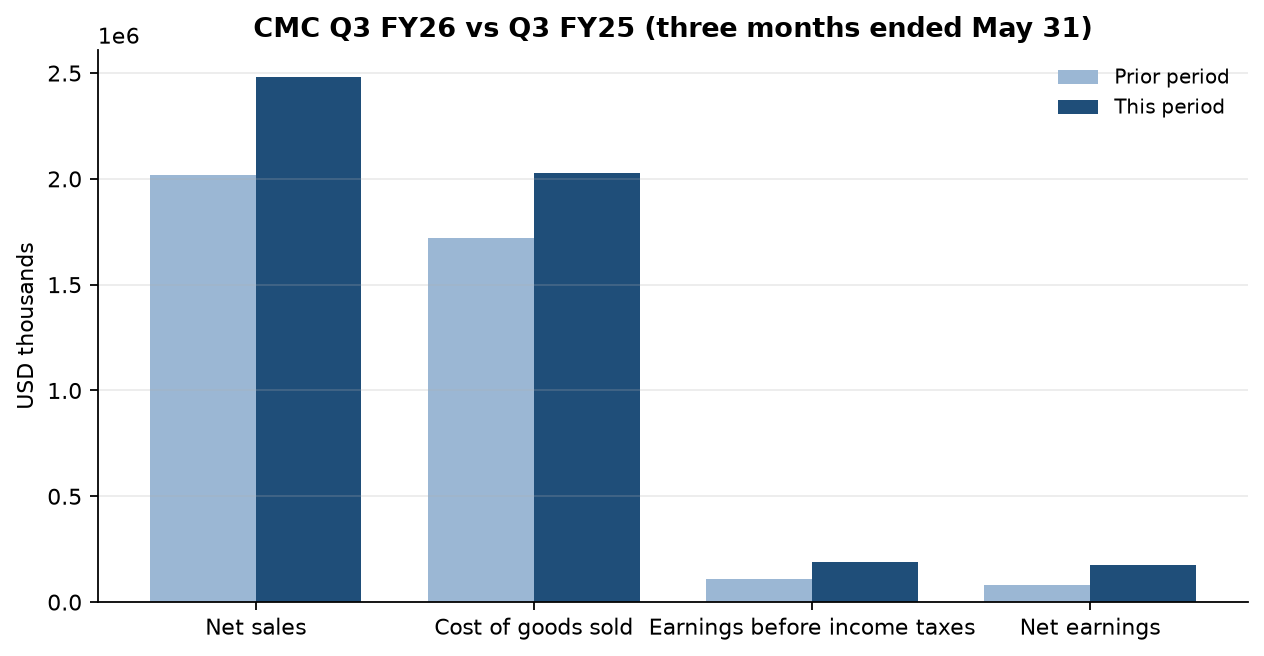

On the surface this is a blowout quarter. Nine-month net earnings of $443.3M ($4.00 basic EPS) reverse a prior-year $67.1M loss, and Q3 net sales rose ~23% to $2.48B with net income more than doubling to $173.0M. The market will read it as a clean operating turnaround.

Most of the year-over-year swing, though, is non-operational. The prior-year nine-month loss was manufactured by a $358.5M litigation charge; this year's was just $11.6M — that one line explains roughly $347M of the $567M improvement in pretax earnings. A 7.9% nine-month effective tax rate (well below a normal corporate rate) and Poland energy subsidies booked into cost of goods sold ($36.0M, down from $48.1M) flatter the result further. The underlying engine did improve — Q3 sales grew ~23% against ~18% cost-of-goods growth, so gross margin widened — but the reported profit overstates how much of that is durable.

The real story is the balance sheet. CMC spent ~$2.5B in cash on Foley ($1.84B) and CP&P ($675M) to build a precast platform, funding it with ~$2.0B of new 5.750%–6.000% notes. Long-term debt jumped 2.5x to $3.31B, goodwill ballooned 5.5x to $2.14B (about 22% of total assets, with $1.33B of Foley's price alone landing as goodwill), cash halved to $559.8M, and quarterly interest expense quadrupled. The company traded a fortress balance sheet for a leveraged bet on precast.

What to watch: whether the acquired precast margins justify $2.1B of goodwill (purchase accounting is still preliminary and could be revised), where the effective tax rate settles as the benefit normalizes, and the still-unresolved $373.5M litigation accrual sitting on the balance sheet.

Want this on every stock you own?

Run instant AI analysis of any 10-K or 10-Q from EDGAR — major risks, red flags, cash flow quality, and moat — with Value of Stock Premium.

This analysis is generated from the filing text and is for educational purposes only — not financial advice. Always do your own research before investing.