Daktronics ($DAKT): A Record $356M Backlog Hides the Real Variable — Tariff-Exposed Margins and a Quiet Pivot to Mexico and Micro-LED

The backlog grew to a record $356.2M, but the variable that actually decides the next two years is landed cost, not demand — China-sourced LEDs/PCBs/ICs and tariffs sit between a healthy order book and the cash it converts to. The Mexico plant (fiscal 2027) and the micro-LED XDC acquisition are the company quietly trying to take back control of its own cost and technology curve.

DAKT

10-KCautiousDaktronics, Inc.

The backlog grew to a record $356.2M, but the variable that actually decides the next two years is landed cost, not demand — China-sourced LEDs/PCBs/ICs and tariffs sit between a healthy order book and the cash it converts to. The Mexico plant (fiscal 2027) and the micro-LED XDC acquisition are the company quietly trying to take back control of its own cost and technology curve.

⚠ Major Risks

- •Tariff and trade-policy exposure: roughly 80% of output is manufactured in the U.S. but depends on components (LEDs, printed circuit boards, integrated circuits) sourced disproportionately from China across a 40+ country supply web, with U.S. tariff rates the filing calls 'elevated' and Canada adding retaliatory duties on exports — a direct hit to cost of goods.

- •Supply-chain concentration: certain proprietary materials come from single- or limited-source suppliers, so loss of a key supplier, part unavailability, or transport disruption could halt production.

- •Cyclicality, seasonality and lumpy project revenue: results swing on large 'uniquely configured' orders (pro sports, spectacular commercial projects); the fiscal third quarter is structurally weaker, and competitively bid uniquely configured orders carry lower gross margins.

- •Liquidity and capital-access dependence: management's own forward-looking statements repeatedly flag adequate liquidity, the potential need to seek additional debt or equity capital, 'strategic alternatives,' and the ability to fund obligations and working-capital needs.

- •Intense competition and commoditization: low-cost domestic and foreign rivals, some with more capital and government funding, plus competition from other ad media; management states the business is not materially dependent on its patents, so product features can be copied.

🔍 Accounting Red Flags

- ▲Over-time (percentage-of-completion) revenue recognition on uniquely configured orders relies on management estimates of progress, with retainage on construction-type contracts and finance receivables extended to customers — an inherently estimate-heavy, working-capital-intensive model to scrutinize (no restatement or error-correction boxes were checked, and Deloitte issued a 404(b) attestation).

- ▲Valuation of, and advances to, affiliates: convertible-debt advances to Miortech (a consolidated variable interest entity) and to XDisplay/XDC; the filing explicitly lists 'the valuation of investment in and advances to affiliates' as a risk — hard-to-value, related-party-adjacent exposures.

- ▲Goodwill created/reallocated by the December 2025 XDC acquisition across the Live Events, Commercial and Transportation segments, with management flagging 'any future goodwill impairment charges' as a forward-looking risk.

- ▲Related-party financing footprint: a 2023 related-party convertible note offering and related-party transactions (e.g., Milwaukee Bucks) warrant governance/related-party scrutiny.

💰 Cash Flow Quality

The business model is structurally working-capital-intensive and management itself foregrounds funding working capital, so cash conversion — not order intake — is the constraint.

- •Percentage-of-completion accounting ties up cash in unbilled receivables, retainage and inventory well before projects convert to collected cash.

- •The Company extends finance receivables to customers and carries retainage on construction-type contracts, lengthening the cash cycle.

- •Seasonality concentrates lower activity in the fiscal third quarter, creating intra-year cash swings.

- •Forward-looking statements emphasize 'ability to increase cash flow to support operating activities and fund its obligations and working capital needs,' plus potential need for additional debt or equity capital — an unusual emphasis alongside a record backlog. (Cash-flow-statement figures were not included in the provided excerpt.)

🏰 Competitive Position

Scale, brand, vertical integration and a large North American installed base give Daktronics a real but narrowing edge over commoditizing LED hardware.

- +Vertically integrated lifecycle (design, engineering, manufacturing, installation, service and long-term maintenance/upgrade/replacement) that locks in recurring service and replacement revenue.

- +Established brands and platforms (Daktronics, All Sport, Galaxy, Vanguard, Venus Control Suite, Show Control, Camino) and a broad product range spanning sports, OOH advertising and transportation.

- +Direct sales force plus global reseller/AV-integrator network, general-contractor licenses in many jurisdictions, and predominantly U.S.-based manufacturing useful for government/transportation buyers.

- +Software/control-system stickiness (cloud-capable VCS, Show Control, Camino) layered on the hardware.

- -Core LED display hardware is increasingly commoditized as technology costs decline; management says the business is not materially dependent on its patents — competitors can copy features.

- -Exposure to lower-cost foreign competitors and rivals with more capital and government funding.

- -Project-based, competitively bid 'uniquely configured' orders carry lower and more volatile gross margins.

- -China-dependent component supply chain leaves the cost base hostage to tariffs and trade policy.

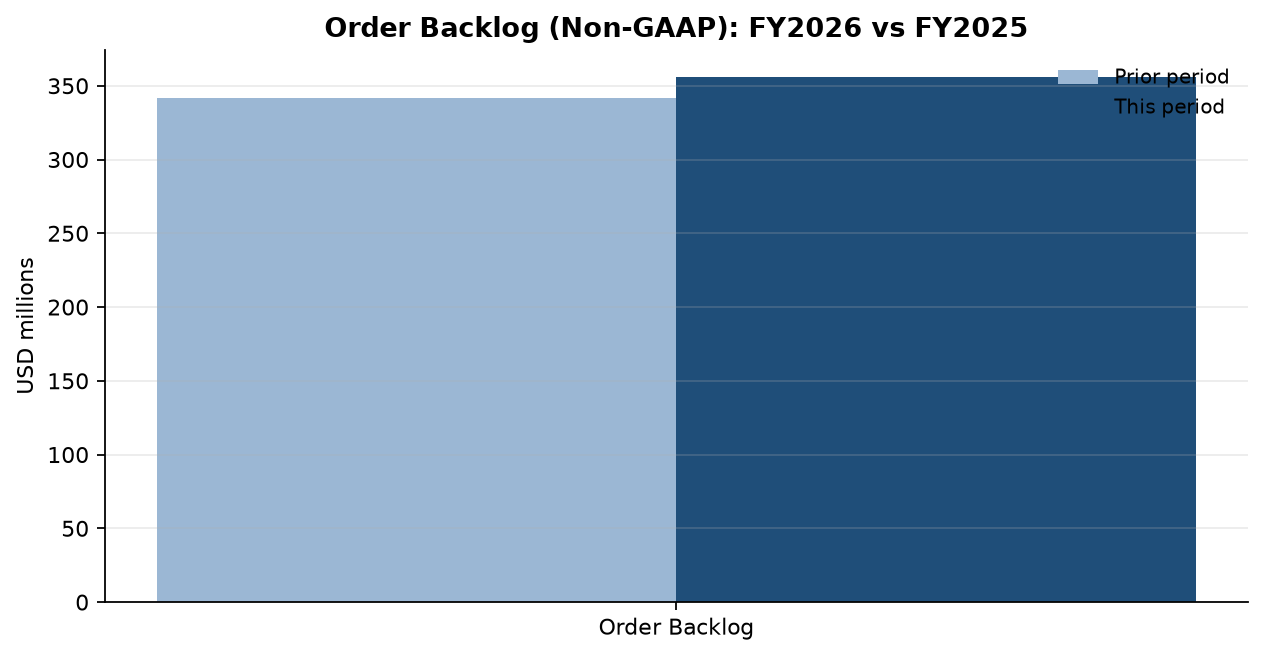

The easy read on Daktronics is a steady industrial: order backlog edged up to $356.2 million from $341.6 million, the secular shift from static to LED signage keeps marching, and a vertically integrated franchise still owns the North American sports and transportation venue. Boring, cyclical, fine.

The number that actually decides the next two years isn't backlog — it's landed cost. Daktronics makes roughly 80% of its output in the U.S. but feeds those plants with LEDs, printed circuit boards and integrated circuits sourced disproportionately from China, across a 40-plus-country supply web, into a tariff regime the filing itself calls 'elevated' and unsettled, with Canada adding retaliatory duties on the way out. A scoreboard maker's moat was never the patents — management flatly says the business isn't materially dependent on them; it's scale and service. Tariffs attack the one cost variable scale doesn't fix, and they bite hardest on competitively bid, lower-margin 'uniquely configured' projects. That is why the two quiet moves in this filing matter more than the order book: a new Mexico plant slated for fiscal 2027 to nearshore the cost base, and the December 2025 acquisition of micro-LED developer XDC to buy down the next technology curve.

Read the forward-looking section as a tell, not boilerplate. Management keeps 'adequate liquidity,' 'seeking additional debt or equity capital,' 'strategic alternatives,' and 'fund its obligations and working capital needs' on the page — unusual emphasis for a company posting a record backlog, and a hint that the percentage-of-completion model ties cash up in receivables, retainage and inventory long before projects convert. A refinanced revolver (November 2025) and related-party convertible notes are the bridge; convertible-debt advances to affiliates (Miortech, XDC) are cash flowing the other way.

Watch gross margin against backlog, not backlog alone. If orders keep climbing while margins erode under tariffs and bid competition, the record book becomes low-quality revenue that consumes working capital; if the Mexico plant and parts standardization hold the line, that same backlog drops through to cash. The swing factor here is whether Daktronics controls its own cost of goods — not whether customers want the displays.

Want this on every stock you own?

Run instant AI analysis of any 10-K or 10-Q from EDGAR — major risks, red flags, cash flow quality, and moat — with Value of Stock Premium.

This analysis is generated from the filing text and is for educational purposes only — not financial advice. Always do your own research before investing.