Ennis, Inc. ($EBF): Q1 sales 'growth' is all M&A — the filing's own pro forma shows revenue actually fell ~2.4% as the core print business keeps eroding

The steady headline — sales up 1.5%, EPS up a penny, cash piling up — hides that all the growth was bought: strip out the NEC/ESS and CFC acquisitions and the filing's own pro forma shows sales down ~2.4% and net earnings lower, so the dividend and a $107M goodwill load now rest on a still-shrinking organic base.

EBF

10-QCautiousEnnis, Inc.

The steady headline — sales up 1.5%, EPS up a penny, cash piling up — hides that all the growth was bought: strip out the NEC/ESS and CFC acquisitions and the filing's own pro forma shows sales down ~2.4% and net earnings lower, so the dividend and a $107M goodwill load now rest on a still-shrinking organic base.

⚠ Major Risks

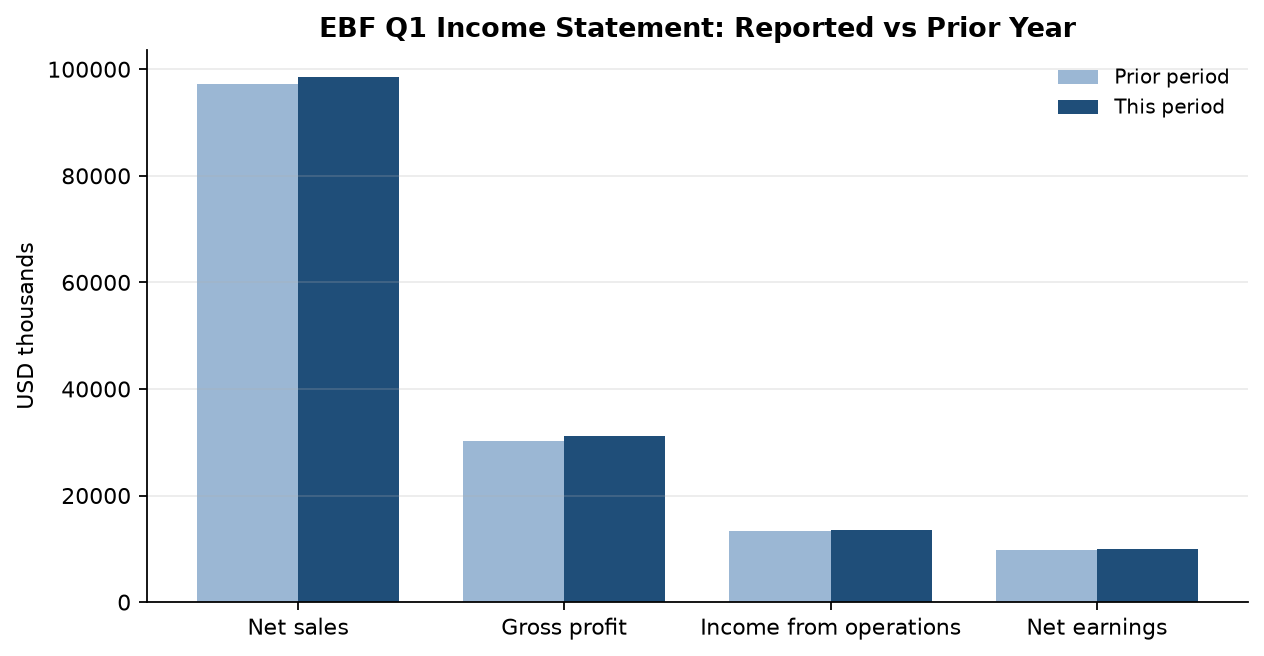

- •Secular decline in demand for traditional printed business forms from digital substitution and product obsolescence — on a pro forma (ex-acquisition) basis, net sales fell from $101,059K to $98,615K year over year.

- •Paper-supply concentration and volatility: the Company buys paper 'primarily from one major supplier,' and the sole domestic producer of carbonless paper permanently closed its plant in fiscal 2026, forcing alternative sourcing and inventory build.

- •Margin pressure from input-cost inflation, tariffs, trade regulations and freight in what management itself calls an 'already over-supplied, price-competitive print industry.'

- •Acquisition dependence and integration risk — top-line stability rests on serial M&A ($35.0M for NEC/ESS in April 2025, $3.9M for CFC in Nov 2025), leaving $106.6M of goodwill (34% of equity) exposed to impairment if volumes or margins slip.

- •High cash payout on a flat-to-declining earnings base — a $0.25 quarterly dividend (~65% of net earnings, ~5.3% yield per the option-pricing assumptions) plus $48.6M of cash held above FDIC-insured limits.

🔍 Accounting Red Flags

- ▲Reported +1.5% sales growth masks an organic decline: the filing's own pro forma disclosure shows sales would have fallen ~2.4% ($101,059K to $98,615K) and pro forma net earnings dropped ($10,151K to $9,879K) had the acquisitions been owned in both periods.

- ▲Equity-to-liability modification of stock awards: in April 2026 the Compensation Committee approved cash settlement of certain RSUs, reclassifying ~$2.2M out of additional paid-in capital into accrued compensation liabilities — an unusual comp restructuring whose future value changes now run through expense.

- ▲Capital expenditures collapsed to just $352K (from $1,368K a year earlier), flattering free cash flow and hinting at deferred investment in a capital-intensive manufacturing base.

- ▲Goodwill ($106.6M) plus net intangibles ($36.8M) equal ~46% of shareholders' equity, tested only qualitatively as of Dec 1, with no impairment taken despite management's acknowledged 'continued declines in demand.'

💰 Cash Flow Quality

Cash generation is genuinely strong and debt-free, but the eye-catching year-over-year jump is working-capital-driven rather than earnings-led.

- •Operating cash flow rose to $21,232K from $7,960K, but the swing came from working capital — receivables provided $3,957K (vs a $7,340K use) and prior-year cash was depressed by an $11,798K acquisition-related inventory build — not from earnings growth (net earnings were roughly flat at $9,879K vs $9,799K).

- •Earnings are well-backed by cash, with ~$4.2M of D&A add-backs and minimal earnings-to-cash gap.

- •Capex of only $352K flatters free cash flow and may signal underinvestment.

- •Cash rose to $49,082K with essentially no debt (only ~$0.2M in standby letters of credit); the $6,378K dividend and paused buyback were easily covered.

🏰 Competitive Position

Ennis is the largest US supplier of business forms, labels, envelopes and folders to independent distributors — real scale in a structurally shrinking, over-supplied niche.

- +Management believes it is the largest producer of business forms, pressure-seal forms, labels, tags, envelopes and presentation folders sold through independent distributors in the US.

- +Scale and geographic breadth — roughly 50 manufacturing plants across 20 states — plus buying power with paper suppliers.

- +Broad multi-brand portfolio and entrenched independent-distributor relationships; ~95% custom/semi-custom products.

- +Clean, net-cash balance sheet ($49.1M cash, negligible debt) that funds bolt-on acquisitions.

- -End market is in secular decline as digital distribution, print-on-demand and lower-cost grades displace traditional forms.

- -Limited pricing power in a 'highly price-competitive and volatile' market; margins exposed to paper cost swings.

- -Dependence on a limited number of paper suppliers, underscored by the closure of the sole domestic carbonless-paper producer.

- -Growth is acquisition-reliant, adding goodwill/intangibles that must earn their keep in a declining industry.

The consensus read on EBF is a boring, reliable dividend payer: net sales edged up to $98.6M, diluted EPS ticked to $0.39, operating cash flow nearly tripled to $21.2M, and the balance sheet holds $49M of cash with essentially no debt. On the surface, another dependable quarter.

Invert it using the company's own numbers. Ennis bought NEC/ESS ($35.0M, April 2025) and CFC ($3.9M, Nov 2025); back those out and the pro forma table shows sales would have fallen from $101.1M to $98.6M — roughly -2.4% — with pro forma net earnings down from $10.2M to $9.9M. The reported 'growth' is acquired, not earned. The legacy business-forms core is still eroding exactly as the MD&A's own language on digital substitution and 'continued declines in demand' admits. This is an acquisition treadmill: buy small printers to paper over the shrinkage of the existing book. It works while the balance sheet is clean and targets are cheap, but each deal stacks goodwill — now $106.6M, about a third of assets and a third of equity — that must keep earning in a declining industry.

Two tells sit under the hood. Capex was cut to just $0.35M from $1.37M, which flatters free cash flow in a business management itself calls over-supplied and price-competitive — cheap now, but not a lever you can pull forever. And in April 2026 the comp committee converted a slug of stock awards to cash settlement, moving ~$2.2M out of paid-in capital into liabilities — trading dilution for future cash outflow and expense volatility.

The one thing to watch: whether organic (ex-acquisition) sales stabilize or the pro forma decline steepens — and whether the annual December 1 goodwill test on that $107M starts to bite if volumes keep sliding. The paused buyback (zero repurchases this quarter versus $5.0M a year ago) suggests management is already husbanding cash.

Want this on every stock you own?

Run instant AI analysis of any 10-K or 10-Q from EDGAR — major risks, red flags, cash flow quality, and moat — with Value of Stock Premium.

This analysis is generated from the filing text and is for educational purposes only — not financial advice. Always do your own research before investing.