Kewaunee Scientific ($KEQU): A Full Year of Nu Aire Masks a 23% Backlog Collapse Heading Into FY2027

FY2026 results almost certainly benefited from a full year of Nu Aire (versus roughly a half year in FY2025), but the order backlog — the firm's best leading indicator since products ship into buildings yet to be built — shrank ~23%. The acquisition is flattering a contracting forward book.

KEQU

10-KCautiousKewaunee Scientific Corporation

FY2026 results almost certainly benefited from a full year of Nu Aire (versus roughly a half year in FY2025), but the order backlog — the firm's best leading indicator since products ship into buildings yet to be built — shrank ~23%. The acquisition is flattering a contracting forward book.

⚠ Major Risks

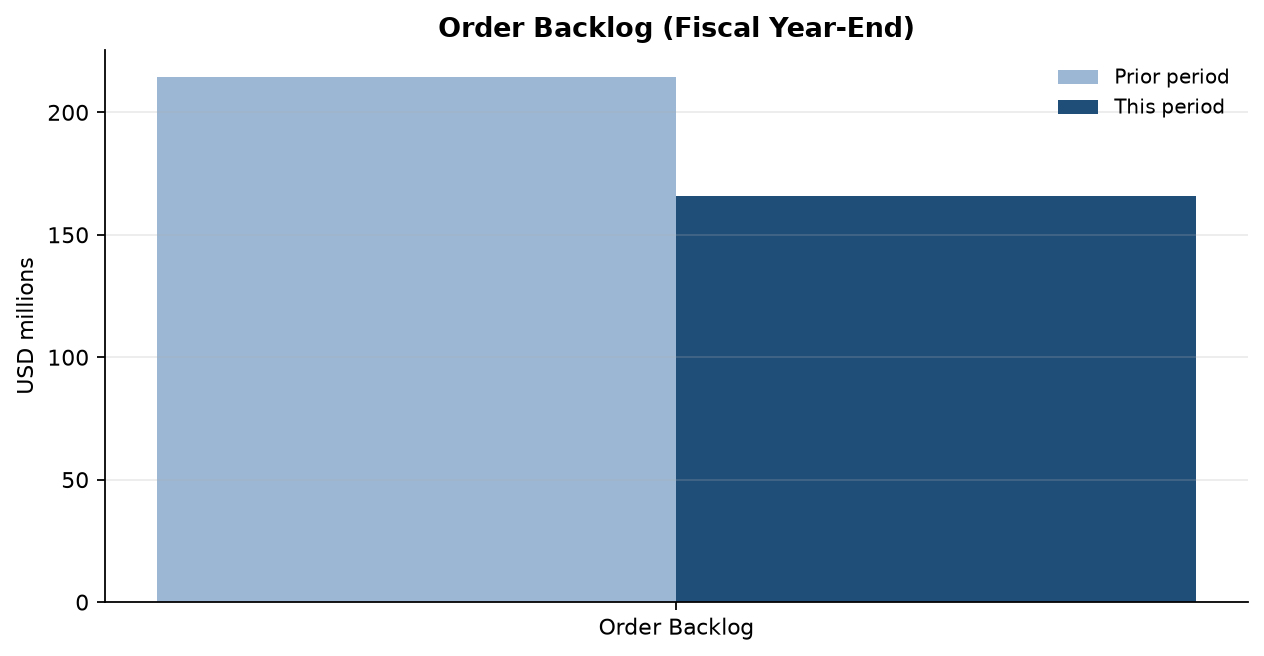

- •Order backlog fell to $165.9M at April 30, 2026 from $214.6M a year earlier (a ~$48.7M, ~23% drop), pointing to a softening forward revenue pipeline even though management expects ≥90% of it to ship in FY2027.

- •Heavy customer concentration: two domestic dealers plus the national stocking distributor were ~34% of FY2026 sales (41% in FY2025); loss of any one would materially hit revenue and profit.

- •Nu Aire integration and impairment exposure: the November 2024 acquisition was debt-funded (seller notes, Term Loan B, revolving facility, amended loan agreements) and carries goodwill and acquired intangibles the company explicitly flags as impairment-prone.

- •Firm-price quotes on long-lead construction orders leave the company bearing raw-material and tariff inflation (steel, stainless, wood, epoxy resin) between quote and delivery, with no guarantee it can raise prices to match.

- •Cyclical end-market and funding risk: revenue depends on lab/healthcare construction activity and government research funding, with 28% of FY2026 revenue from outside the U.S. (FX, geopolitical, and trade-policy exposure).

🔍 Accounting Red Flags

- ▲Revenue-timing judgment: significant over-time recognition tied to construction projects, plus retention amounts collected only at project completion, makes reported sales and working capital sensitive to project timing and management estimates.

- ▲Goodwill and acquired intangibles from Nu Aire create future impairment risk that management warns could be material if demand keeps softening (consistent with the falling backlog).

- ▲2022 sale-leaseback of the Statesville manufacturing/office facilities converted owned real estate into long-term lease obligations — a financing structure that should be examined alongside the debt stack.

- ▲No independent auditor attestation on internal control over financial reporting (the Section 404(b) box is unchecked) — permitted as a smaller reporting / non-accelerated filer, but it means ICFR is management-assessed only.

💰 Cash Flow Quality

The full cash-flow statement is outside the provided excerpt, but the disclosed model — retention-heavy, long-DSO collections layered on a debt-funded acquisition and a declining backlog — points to a working-capital-intensive, leveraged cash profile.

- •Management states payments are typically received in the quarter following shipment, with retention amounts held until final project completion, structurally inflating required working capital.

- •A listed risk is 'failing to generate sufficient future positive operating cash flows and, if necessary, secure and maintain adequate external financing.'

- •Acquisition and operations are supported by a multi-layer debt stack (seller notes, Term Loan B, revolving credit facility, amended loan agreements) plus a 2022 sale-leaseback.

- •A ~23% backlog decline implies softer future shipments and collections unless bookings recover.

🏰 Competitive Position

A 120-year-old niche brand with genuine specification and channel advantages, but one that competes heavily on price through public bidding, which caps pricing power.

- +Long-established brand (founded 1906) with architect/engineer specification influence that creates switching friction on projects.

- +Nu Aire is described as a recognized market leader in biological safety cabinets and airflow products, broadening the portfolio into life-sciences equipment.

- +Established dealer/distributor channel plus international subsidiaries in Singapore, India, Spain and Saudi Arabia.

- -A significant portion of business is won via competitive public bidding where price is a principal deciding factor.

- -Customer concentration (~34% via three channel partners) limits negotiating leverage.

- -Company concedes success is not dependent on patents/licenses, underscoring limited proprietary protection.

- -Micro-cap with thin float (2,870,410 shares, ~$70M non-affiliate market value, only 82 holders of record), implying low liquidity and high volatility.

The consensus read is straightforward: a 120-year-old lab-furniture maker bought Nu Aire, a recognized leader in biosafety cabinets, and is consolidating its way toward 'market leader' status — combined revenue is bigger and the story is intact. The numbers in the front half of this filing invert that. The single most predictive figure here is order backlog, because Kewaunee books revenue as it ships product into buildings that are often still under construction. That backlog fell from $214.6 million to $165.9 million — a roughly $48.7 million, ~23% decline in one year.

With a full year of Nu Aire now in the base (versus only a partial year in FY2025), the headline top line is doing what acquisitions do: it papers over a forward order book that is actually contracting. In plain English, the company is shipping out a backlog it built in prior years while refilling it more slowly. That matters more than usual because of how this business converts to cash: firm-price quotes expose it to raw-material and tariff inflation, and retention-heavy, quarter-lagged collections tie up working capital — all sitting on top of a debt-funded acquisition (seller notes, a Term Loan B, a revolver, and a 2022 sale-leaseback).

Two structural fragilities compound it: ~34% of sales run through just three channel partners, and this is a thin-float micro-cap (about 2.87 million shares, ~$70 million in non-affiliate value, 82 holders of record) that wins much of its work via price-based public bidding. The thing to watch into FY2027 is bookings: if the backlog keeps sliding, the next pressure point is a goodwill or intangible impairment on Nu Aire, which management has already flagged as a real possibility. Note that the income statement, balance sheet and cash-flow statement were beyond the text provided, so this read is built on the operational and risk disclosures rather than the audited financials.

Want this on every stock you own?

Run instant AI analysis of any 10-K or 10-Q from EDGAR — major risks, red flags, cash flow quality, and moat — with Value of Stock Premium.

This analysis is generated from the filing text and is for educational purposes only — not financial advice. Always do your own research before investing.