Universal Safety Products ($UUU) Sold Its Only Real Business — and Its Crypto Pivot Owes an Insider-Linked Firm Up to $93.75 Million Before Shareholders Win

This is no longer a safety-products company — it sold that business, its brands, and its name. The upside case is now a related-party crypto bet in which an insider-linked entity holds a contractual first claim of up to $93.75 million on the venture's proceeds — more than ten times the entire market value of the stock held by outside shareholders.

UUU

10-KBearishUniversal Safety Products, Inc.

This is no longer a safety-products company — it sold that business, its brands, and its name. The upside case is now a related-party crypto bet in which an insider-linked entity holds a contractual first claim of up to $93.75 million on the venture's proceeds — more than ten times the entire market value of the stock held by outside shareholders.

⚠ Major Risks

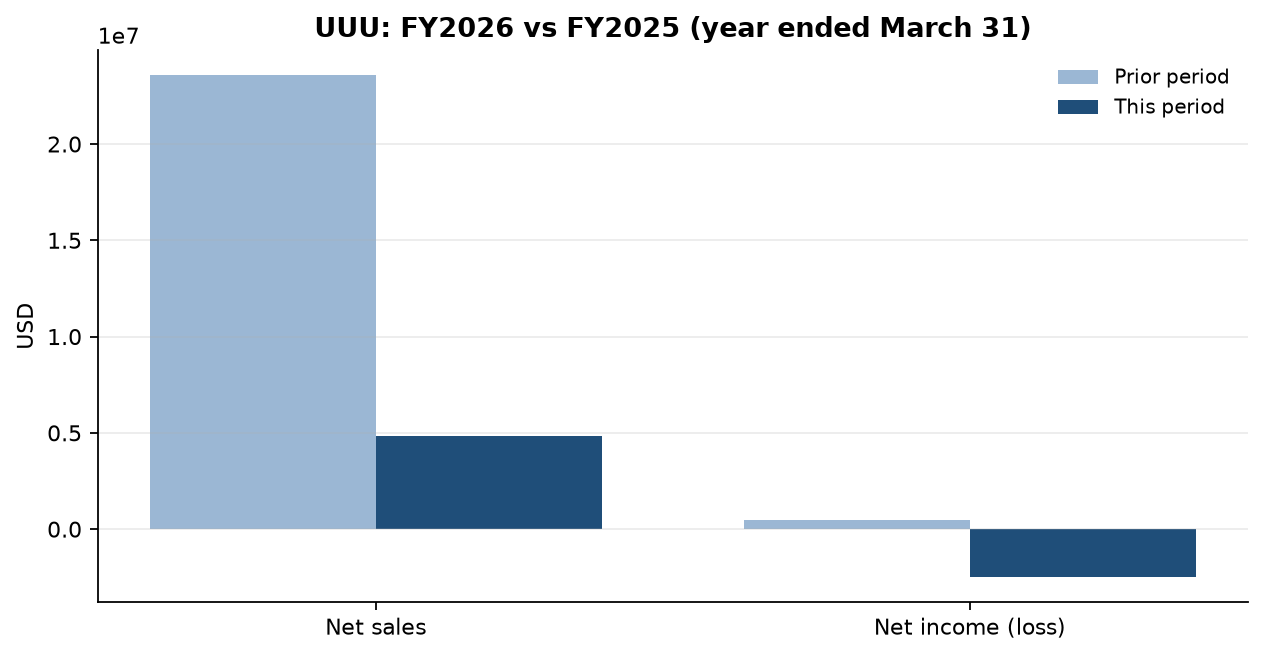

- •The core smoke/carbon-monoxide alarm business — and the company's own trade names — were sold to Feit Electric in May 2025: sales collapsed from $23.6M to $4.8M and order backlog went from ~$2.14M to exactly $0 at fiscal year end.

- •The DeFi pivot has no revenue and no operating history: the tokenization platform has not launched, and Universal DeFi 'does not currently generate cash revenue and expects to depend on outside funding to support its operations for the foreseeable future.'

- •Both new business lines depend entirely on the Ault Blockchain, a brand-new, unproven network developed by an organization affiliated with UUU's own Executive Vice Chairman — concentrated exposure the filing itself flags as a conflict of interest.

- •The ~425 million AULT tokens earned have no current market value, are non-cash and illiquid, and 'may never have value'; the validator's staked tokens can also be slashed for downtime, double-signing, or misconfiguration.

- •What remains of the legacy import business is fragile: Eyston (China) supplied 82.6% of FY2026 purchases, certain products carry 25% tariffs, and the filing describes tariff policy as unprecedented and unstable.

🔍 Accounting Red Flags

- ▲Related-party asset transfer at the heart of the pivot: the 125,000 node licenses and the validator were transferred from Ault Capital Group, a subsidiary of Hyperscale Data — whose Executive Chairman, Milton C. Ault, III, is UUU's Executive Vice Chairman; Ault DAO's CEO, Henry Nisser, sits on UUU's board.

- ▲The Revenue Sharing Agreement (signed June 30, 2026 — two days before this 10-K was filed) entitles the affiliate to 25% of net proceeds until it has collected a cumulative $93,750,000, versus an $8.4 million aggregate market value for all non-affiliate shares.

- ▲UUU's validator is operated day-to-day by the affiliate with no executed agreement; the filing concedes the arrangement 'is not the result of arm's-length negotiation' and that costs and terms are not fixed.

- ▲Tokens earned generate 'no recognizable asset or revenue' today; revenue would be recognized only if a market for AULT ever develops, followed by quarterly fair-value remeasurement — earnings quality would then hinge on marks for a thinly traded affiliate-created token.

- ▲XBRL tagging discloses a convertible debenture issued August 2025 carried with Level 3 embedded-derivative fair-value inputs and further subsequent-event activity in June 2026 — dilutive financing whose note-level terms deserve close reading.

💰 Cash Flow Quality

The cash-generating alarm business is gone, the remainder swung to a $2.5M net loss with zero backlog, and the new venture explicitly expects to live on outside funding while earning only non-cash tokens the company says have no market value.

- •Net loss of $2,485,763 in FY2026 versus net income of $500,684 in FY2025 — a $2,986,447 swing the company attributes primarily to the Feit sale.

- •Order backlog fell from approximately $2,142,000 to $0 at March 31, 2026, so there is no revenue visibility entering FY2027.

- •Universal DeFi 'does not currently generate cash revenue and expects to depend on outside funding'; node and validator rewards are non-cash, illiquid tokens with no current market value.

- •Convertible debenture financing (issued August 2025, with subsequent-event activity in June 2026 per the filing's XBRL) signals the cash gap is being bridged with potentially dilutive paper.

🏰 Competitive Position

UUU sold its brands, its alarm line, and even its corporate name; what's left is a seven-employee importer of commodity electrical products plus a pre-revenue crypto venture wholly dependent on an affiliate's unproven blockchain.

- +Remaining distribution infrastructure: ~40 independent sales organizations and regional stocking warehouses for the electrical products line.

- +Owns 125,000 of a fixed 1,000,000 Ault Blockchain node licenses (12.5% of the network's mining-node emissions base) plus a validator — meaningful optionality if, and only if, the network ever gains real value.

- -No proprietary brand left — the Universal Security Instruments and Universal Electric trade names were sold to Feit with the alarm business.

- -82.6% of purchases come from a single Chinese manufacturer, with certain products subject to 25% tariffs.

- -No in-house DeFi experience: the filing states the entire pivot relies on the personal expertise of one executive, Milton C. Ault, III.

- -The tokenization platform has not launched and faces larger, better-resourced competitors; the filing warns the business model itself 'may change materially.'

The consensus read writes this off as a transition year: a micro-cap sells its legacy smoke-alarm unit to Feit Electric, books a one-time $2.5 million loss, and reinvents itself as a blockchain play. The filing encourages that framing — the loss is 'attributed primarily to the sale' — and the DeFi story supplies the go-forward narrative.

Follow where the value actually flows and the story inverts. Universal DeFi didn't build its crypto operation; it received 125,000 node licenses and a validator from Ault Capital Group, a subsidiary of Hyperscale Data — whose Executive Chairman, Milton C. Ault, III, is simultaneously UUU's Executive Vice Chairman. In exchange, UUU owes the affiliate 25% of all net proceeds until the affiliate has collected a cumulative $93,750,000. For scale: every share of UUU held by outsiders was worth $8.4 million combined at the last measured date. If the Ault Blockchain fails, shareholders own roughly 425 million tokens the company itself says have no market value and may never have any. If it succeeds, an insider-linked entity is contractually positioned to skim a quarter of the winnings up to a ceiling more than ten times the public float's value. The risk sits with UUU holders; a large slice of the reward is routed to the affiliate by contract.

And the old business is not a fallback. Sales fell 79% to $4.8 million, year-end backlog is literally zero, the company sold its own trade names, and the surviving import operation runs on seven employees with 82.6% of purchases coming from one Chinese supplier behind 25% tariffs. Meanwhile the validator — one of the two DeFi revenue engines — is being run day-to-day by the same affiliate under a handshake arrangement the filing admits is not arm's-length, with no signed contract and unfixed costs.

The one thing to watch: whether AULT tokens ever trade at a real, observable market price. Until then, every 'reward' UUU earns is a bookkeeping nullity — no revenue, no asset — while operating losses get financed with dilutive paper like the August 2025 convertible debenture. And if the tokens ever do trade, watch how much of the realized cash actually reaches UUU shareholders after the affiliate's 25% takes its cut.

Want this on every stock you own?

Run instant AI analysis of any 10-K or 10-Q from EDGAR — major risks, red flags, cash flow quality, and moat — with Value of Stock Premium.

This analysis is generated from the filing text and is for educational purposes only — not financial advice. Always do your own research before investing.